2026 Guide to Automated Risk Data Capture for MGAs Using AI

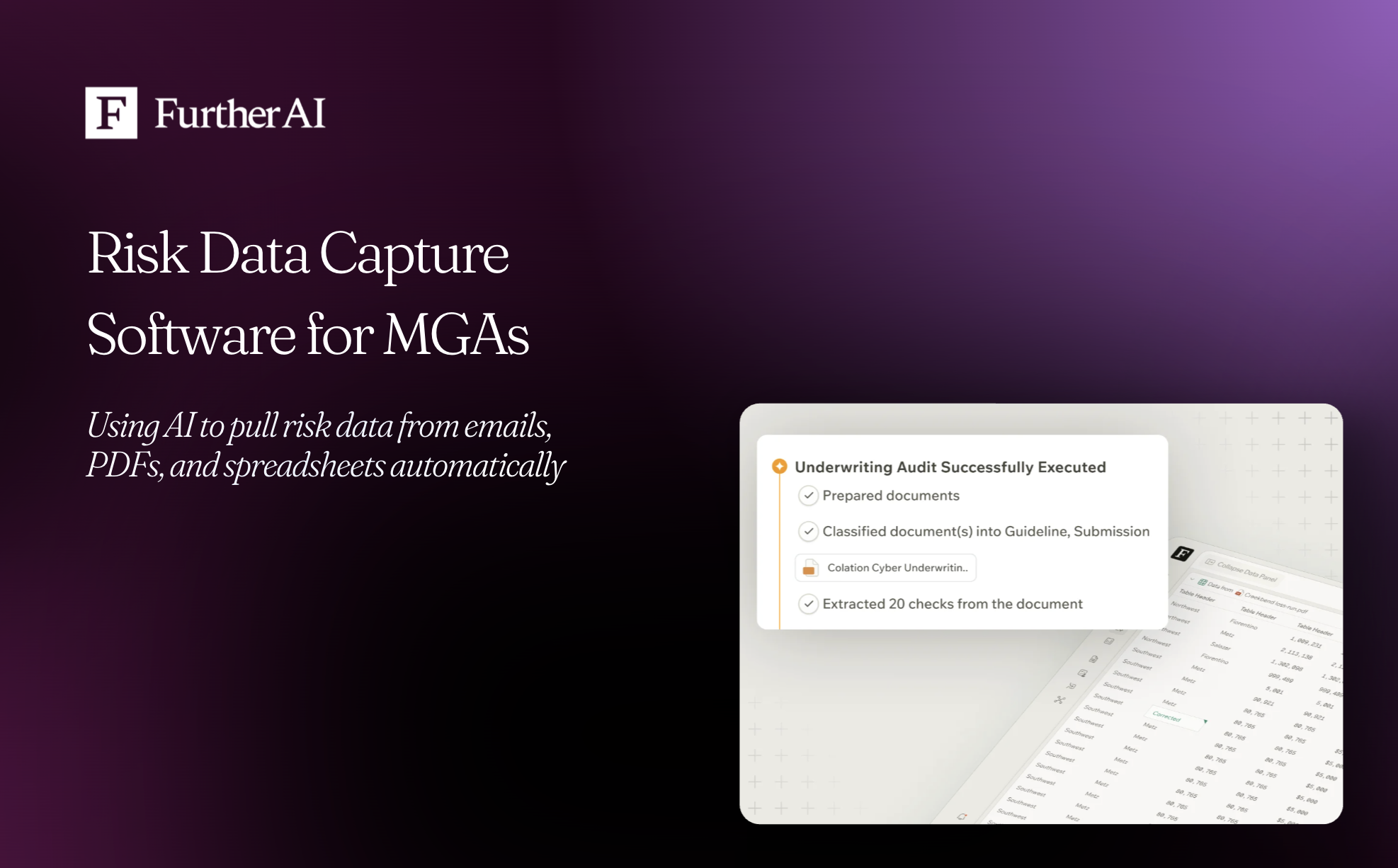

Automated risk data capture is software that reads broker emails, PDFs, spreadsheets, and scanned documents, then extracts and normalizes the underwriting data inside them into structured fields your rating and policy systems can use. For managing general agents (MGAs), it removes the manual re-keying that slows submission intake and introduces errors before an underwriter ever sees the risk.

In this guide, we explain in detail what the technology does, where to start, what to look for in a platform, and how to deploy it safely. It's written for underwriting, operations, and compliance leaders who are looking for measurable results.

Key takeaways

- Automated risk data capture extracts and normalizes risk data from emails, PDFs, spreadsheets, ACORD forms, and loss runs into structured, system-ready fields.

- Submission intake is the highest-leverage place to start because it's high-volume, repetitive, and directly tied to quote turnaround and bind rates.

- McKinsey finds underwriters can spend 30% to 40% of their time on low-value activities like data entry, time automation gives back.

- A majority of MGAs (61.3%) already use AI, but only 35.5% have a formal AI budget, so funding and scope discipline separate the winners.

- Human-in-the-loop review, audit trails, and an AI governance framework are non-negotiable for delegated-authority compliance.

What automated risk data capture means for MGAs

Automated risk data capture is the end-to-end process where software ingests unstructured inputs, identifies the relevant risk details, and outputs clean, structured records. The pipeline typically runs in four stages: ingest the document, extract the fields, normalize them to a standard schema, and route them downstream for review or rating.

For MGAs, the inputs are messy by nature. A single submission can arrive as a broker email with three attachments: a 40-page PDF application, a loss run in one carrier's format, and a statement of values (SOV) spreadsheet with inconsistent column headers. Modern systems combine optical character recognition (OCR), natural language processing (NLP), and large language models (LLMs) to handle that variety, including handwritten notes and imagery that older rules-based tools couldn't read.

The goal is decision-ready data. When intake is structured and verified, underwriters spend their time assessing risk and binding business rather than copying numbers between windows.

Why risk data capture is an MGA priority in 2026

The economics are straightforward. McKinsey & Company found that underwriters can spend 30% to 40% of their time on activities that add little value, such as data entry. Every hour spent on data entry is an hour not spent on underwriting judgment or broker relationships.

MGAs feel this acutely because volume is climbing. AM Best reports that premiums written through MGAs and other delegated underwriting authority enterprises grew by double digits for a fourth consecutive year, reaching roughly $89.9 billion in 2024. Conning's 2025 study confirms the structural shift toward delegated authority. More submissions, the same headcount, and tighter service expectations push intake automation to the top of the list.

Adoption is already broad, but discipline is still rare. In Gallagher Bassett's MGA Market Pulse, 61.3% of MGAs reported using AI while only 35.5% had a formal budget to fund it. That gap predicts the failure modes we see most often: pilots that never reach production and tools shipped half-built that underwriters stop trusting.

Where to start: Use cases and metrics

The best strategy is to start narrow. Pick submission intake for one line of business, define success metrics up front, and measure before you expand. A tight scope reduces technical and change-management risk, lets you iterate faster, and produces a clean business case for the next phase.

Define three metrics before you turn anything on: throughput (volume processed without added headcount), accuracy (both field-level and record-level), and time-to-decision (intake to quotable). These would give you a defensible baseline and a way to prove ROI.

For a deeper look at form-level extraction, see our guide to AI ACORD form data extraction.

Catalog and map your data sources

Before integration, build a data inventory. List every source feeding your underwriting workflow so nothing surfaces as a surprise mid-deployment.

Typical MGA sources include broker emails, ACORD forms, loss runs, SOV spreadsheets, PDFs, handwritten documents, imagery, external data feeds, and third-party data providers. Once you've cataloged them, run a schema-mapping exercise: schema mapping is the process of aligning structured and unstructured input data to a defined standard your policy administration or analytics systems expect.

A simple three-step approach works well:

- Inventory every source and its format, including the messy edge cases.

- Map each extracted field to your target schema and downstream system requirements.

- Flag integration or data-quality gaps early, before they reach production.

What to look for in automated risk data capture software

The strongest platforms are modular and API-first rather than monolithic. That lets you adopt the pieces you need and connect them to the systems you already run. Look for four capabilities working together.

Conversational and context-aware intake captures intent and unstructured signals, not just form fields, which reduces truncation and application errors at the source. LLM-based document extraction handles emails, PDFs, and loss runs across inconsistent formats, including tasks like rebuilding exposure-by-year tables from documents that never agree on layout. Normalization and ETL pipelines convert raw output into your canonical schema. Policy-admin and rating connectors push clean data downstream without a second round of manual entry.

Underwriting outputs are only as reliable as intake data; poor inputs produce wrong downstream decisions. Manual entry is a real source of that risk, with human data-entry error rates running roughly 1% to 4% of fields, as per DigiParser. That's why validation and confidence scoring at the point of capture matter as much as raw extraction accuracy. FurtherAI is built as a modular, multi-model AI workspace for insurance so MGAs can deploy a single workflow or an end-to-end intake pipeline and keep their existing stack.

Keep humans in the loop with audit trails

Human-in-the-loop (HITL) is an operating model where people validate, correct, or approve system outputs before anything moves downstream. For MGAs operating under delegated authority, it's how you keep speed without giving up control.

" When choosing an AI workspace vendor, there are at least three big questions for insurance leaders to consider. Does the vendor orchestrate your existing systems, or want to become a second source of truth? How does the AI behave when it's unsure — pause for a human, or push a confident guess into your policy data? And is governance foundational — audit trails, explainability, editability — or bolted on? Insurance is a regulated industry and you don't want to find out the answers during the first audit." – Danny O’Lenic, Insurance Product Lead at FurtherAI

Build reviewer checkpoints for low-confidence fields, exceptions, and regulatory-sensitive data, and embed them early in every workflow rather than bolting them on later. Pair that with audit trails: full system logging that records each step, change, and review so you can answer carrier and regulator questions with evidence.

Build in AI governance, security, and compliance

A compliance-ready foundation should be in place before you scale. The NIST AI Risk Management Framework offers a structured, voluntary approach to identifying and mitigating AI risks and works well as a baseline for insurance deployments.

From there, layer in the controls a delegated-authority operation needs. The table below summarizes the essentials.

Role-based access control (RBAC) restricts system access to authorized users based on their role. A model inventory is a catalog of all AI models in use, their deployment context, and their oversight status, maintained for auditability.

Pilot, measure, and scale

Treat the rollout as a measured progression, not a big-bang launch:

- Pilot on a narrow use case, such as submission intake for one line of business.

- Measure throughput, accuracy, and time-to-decision against your baseline.

- Monitor for false positives and false negatives, and watch low-confidence trends.

- Expand to adjacent lines and use cases only after results stabilize.

As you scale, run champion-challenger comparisons and continuous monitoring to catch drift, bias, or quality degradation before it reaches underwriters. Report KPIs by phase in a simple dashboard so leadership can see the trajectory. Keep a compliance-ready artifact set throughout: model inventory, decision rationale, audit logs, and reviewer evidence for future regulatory review.

What results MGAs are seeing with FurtherAI

The numbers below come from FurtherAI customer deployments, and they show what disciplined automation produces in practice.

In that submission-processing deployment, a top U.S. MGA with over $1.5 billion in premiums cut average time to clear a submission from about 32 minutes to roughly one minute, a 30x speedup, with close to 100% accuracy. Within three months the system processed more than $20 billion in total insured value and saved over 2,000 hours of manual effort, as per FurtherAI’s case study.

Across its customer base, FurtherAI has processed roughly $30 billion in premiums across 20+ lines of business in all 50 states, and counts named partners including Upland Capital Group, McGowan Excess & Casualty, and Lynx Specialty, which credited FurtherAI with supporting 35% growth. If you run an MGA, our MGA solutions and renewal automation guide are good next reads.

REFERENCES

AM Best. "Best's Market Segment Report: MGA Premiums Showed Double-Digit Growth for Fourth-Straight Year in 2024." news.ambest.com

Conning. "2025 Managing General Agents Study: Built for What's Next." conning.com

DigiParser. "Manual Data Entry Error Rate: How Many Typos Are Hiding in Your Systems?" digiparser.com

Gallagher Bassett. "MGA Market Pulse: Key Insights for 2026." insurers.gallagherbassett.com

McKinsey & Company. "From Art to Science: The Future of Underwriting in Commercial P&C Insurance." mckinsey.com

National Institute of Standards and Technology. "AI Risk Management Framework." nist.gov

DISCLAIMER

This article is for general informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or other professional advice. The content reflects information available as of the date of publication, and FurtherAI undertakes no obligation to update it as laws, regulations, or AI technologies evolve.

Recent posts

Ready to go further and

transform your insurance ops?

Reclaim your time for strategic work and let our AI Assistant handle the busywork. Schedule a demo to see how you can achieve more, faster.

.svg)