7 No-Code Automated Intake Platforms Every Small MGA Should Consider

Strategic overview

A no-code automated intake platform lets a Managing General Agent (MGA) digitize submission and claims intake (extracting data from broker emails, ACORDs, SOVs, and PDFs, then routing structured records into underwriting workflows) without writing code or hiring developers. For small MGAs, the right platform turns a manual, error-prone process into a fast, auditable, scalable one.

The timing is favorable. Forrester now projects the low-code market will approach $50 billion by 2028, fueled by an AI-driven expansion of citizen development inside large enterprises. The MGA market is growing into that tailwind: U.S. MGA direct premiums written rose 16% in 2024 to an estimated $114.1 billion, outpacing the broader property-casualty market, as per Conning 2025 MGA Study. And the problem these platforms solve is well-documented — Accenture reports that underwriters now spend only 26% of their time on actual underwriting, down from 31% in 2021, with the remainder absorbed by intake, navigation, and administration.

This guide compares the seven no-code intake platforms most relevant to a small MGA in 2026: one insurance-native AI option (FurtherAI), one insurance-specific comparison point (Roots.ai), and five general-purpose automation platforms that small operations commonly evaluate.

What "no-code automated intake" actually means for an MGA

For an MGA, intake is the moment a broker email lands in a shared inbox with an ACORD 125/126, a loss run, a SOV spreadsheet, and three PDFs of supplementals. Automated intake means the platform: (1) reads the email and attachments, (2) extracts structured data into your fields, (3) runs clearance and triage rules, and (4) hands a clean record to an underwriter — or rejects/queues the submission with a reason. "No-code" means a business user configures all of that through a visual interface rather than waiting on engineering.

Two filters matter most when evaluating tools as a small MGA:

- Document intelligence. General orchestration tools (Zapier, Make) connect apps but don't inherently understand insurance documents. Insurance-native tools handle the messy unstructured input that 80% of submissions arrive as.

- Deployment time. "No-code" should mean weeks, not quarters. If a vendor's smallest reference customer took six months to go live, it's not a small-MGA fit.

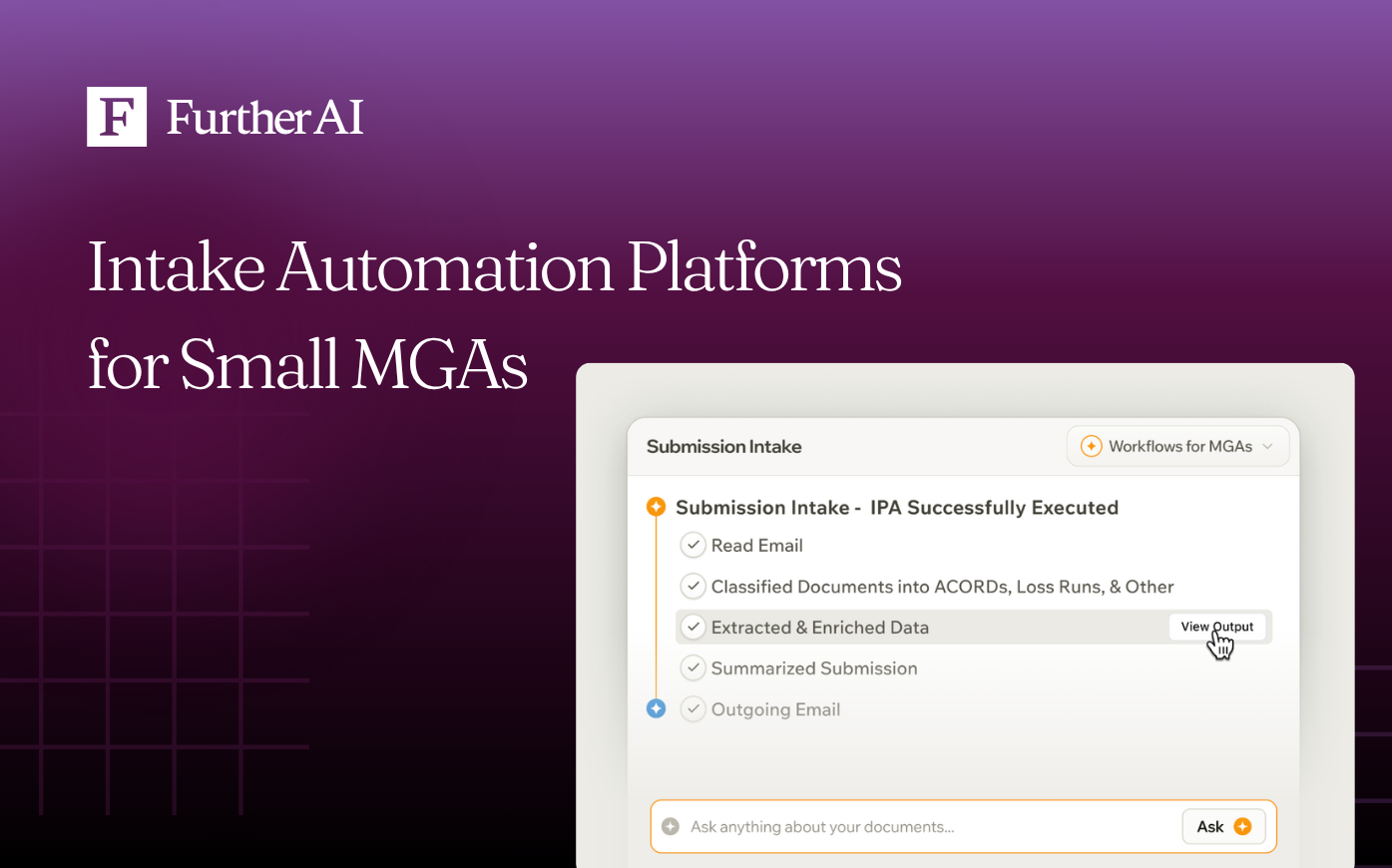

1. FurtherAI — insurance-native AI intake

FurtherAI is built specifically for commercial insurance operations and is the strongest fit for small MGAs that want automated intake without standing up generic orchestration around it. Its domain-trained AI extracts and structures submission data directly from broker emails and attachments, runs eligibility and clearance checks, flags inconsistencies, and routes records into underwriter workflows.

What separates it from general automation tools is that it ships with insurance logic out of the box — ACORD parsing, SOV normalization, loss-run analysis, and policy comparison — rather than requiring an MGA to assemble those capabilities themselves. The platform integrates with policy admin systems, CRMs, and broker portals through pre-built connectors, so a small MGA can typically deploy in days rather than months.

Third-party signals worth noting: FurtherAI raised a $25M Series A led by Andreessen Horowitz in 2025, one of the largest Series A rounds in insurance AI, and counts Accelerant, MSI, and Leavitt Group among its customers.

A published case study documents the specifics: within three months of deployment, FurtherAI's AI Assistant processed over $20 billion in Total Insured Value, saved more than 2,000 hours of manual effort, and delivered a 200% improvement in underwriting efficiency with near-100% data accuracy. Reported intake processing runs roughly 30× faster than the manual baseline.

Best for: Small MGAs that want insurance-aware automation from day one, with built-in audit trails and compliance reporting rather than bolt-on governance.

2. Zapier — easiest starting point for general orchestration

Zapier is where most teams begin when they're moving from spreadsheets to workflows. It connects forms, CRMs, email, and storage across 8,000+ applications, with a learning curve gentle enough that a non-technical operations lead can build their first workflow in an afternoon.

For an MGA, Zapier is useful for the "connective tissue" around intake: piping new web-form submissions into a CRM, posting Slack alerts when a renewal hits a queue, syncing rows between spreadsheets and a policy admin system. Pricing is task-based and predictable at low to mid volumes.

The honest limitation: Zapier doesn't read documents. It moves structured data between apps that already have APIs. If your intake is broker emails with PDF attachments, Zapier alone isn't the answer: you'll pair it with an OCR or AI tool, and at that point an insurance-native platform is usually simpler.

Best for: Lightweight automations around an intake stack you've already built, not the intake itself.

3. Microsoft Power Automate — the right answer if you're a Microsoft shop

If your MGA already runs on Microsoft 365 — Outlook, Teams, SharePoint, Excel, Dynamics 365 — Power Automate is the path of least resistance. It connects natively to those tools plus 1,000+ external systems through standard and premium connectors.

Pricing starts at $15 per user/month for the Power Automate Premium plan, which is required for premium connectors like Salesforce, SQL Server, or Dataverse. Standard Microsoft 365 licenses include only standard connectors, so most MGAs will end up on Premium.

Governance is a strength: role-based access control, audit logging, and Managed Environments make it credible for regulated workflows.

Best for: MGAs already standardized on Microsoft 365 who want one vendor and one identity story.

4. Make (formerly Integromat) — visual logic for branching workflows

Make's canvas-based scenario builder lets you design multi-step automations as a flowchart (with routers, filters, iterators, aggregators, and error handlers), which makes it the better choice when intake logic actually branches: different validations by line of business, conditional triage to different underwriting queues, exception handling that loops back to brokers.

The platform offers 1,800+ pre-built app integrations and over 1,000 templates. It has a steeper learning curve than Zapier but more headroom — most teams that outgrow Zapier's linear "Zap" model land here.

Best for: Small MGAs whose workflows have real conditional logic and want visual control over it without writing code.

5. n8n — self-hosted control for sensitive data

n8n is a fair-code, self-hostable workflow automation platform with 400+ pre-built integrations. "Self-hostable" means you can run the entire platform inside your own infrastructure, so submission data — broker emails, named insureds, claims information — never leaves your security perimeter.

For an MGA with strict data-residency requirements, carrier paper that mandates specific hosting controls, or a privacy-cautious legal team, n8n offers a level of control the SaaS-only platforms can't match. The community edition is free, with a managed cloud tier available for teams that want self-hosting as an option rather than a requirement. The trade-off is operational: someone has to run the infrastructure, and you're working with community support rather than enterprise SLAs.

Best for: Small MGAs with strict data-control requirements or strong technical leadership willing to run the platform.

6. Pipedream — hybrid no-code with optional code

Pipedream sits between fully visual platforms and developer tools. Workflows are built by chaining pre-built steps, but any step can drop into JavaScript, Python, or Go when a no-code action isn't enough — useful when a carrier exposes a quirky API or a rater needs a custom transformation. The platform supports 3,000+ apps with managed authentication.

Pricing is serverless and usage-based, which keeps costs low while volumes are small.

Best for: Small MGAs with one or two technical operators who want no-code speed for 90% of work and a code escape hatch for the rest.

7. Roots.ai (formerly Roots Automation) — insurance-specific alternative

Roots.ai offers AI agents purpose-built for insurance, including submission intake, clearance, and triage from broker emails and attachments. Like FurtherAI, it understands insurance documents natively rather than treating them as generic blobs, and it's a credible option for MGAs that want insurance-aware extraction without building it themselves.

The difference for most small MGAs comes down to scope and deployment model: Roots is positioned around discrete AI "coworkers" for specific tasks, while FurtherAI ships an end-to-end insurance workspace covering intake, policy comparison, audits, and claims under one platform — typically a better fit when a small team needs one tool to cover multiple workflows.

Best for: MGAs evaluating insurance-native automation who want to compare specialist options.

How to choose the right platform for a small MGA

Start with three questions, in this order:

Is your intake primarily documents, or primarily app-to-app data? If broker emails with PDFs and spreadsheets are the bottleneck, the platforms that already understand insurance documents (FurtherAI, Roots.ai) save months versus assembling OCR, extraction, and validation on top of a generic orchestrator. If your data is already structured in upstream systems, a general tool (Zapier, Make, Power Automate) is enough.

What does your existing stack look like? Already on Microsoft 365? Power Automate. Strict data-residency requirements? n8n. Need branching logic across many tools? Make.

What's your real volume in 12 months? Model pricing at 2–3× your current submission volume. Task-based platforms (Zapier, Pipedream) are cheap at low volumes and get expensive at high ones. Per-user platforms (Power Automate) scale predictably with team size. Insurance-native platforms typically price on submission volume or value processed.

Comparison table

Frequently asked questions

What's the difference between an automated intake platform and a general automation tool?

An automated intake platform for insurance reads broker submissions — including unstructured documents like ACORDs, SOVs, and loss runs — and turns them into structured records. A general automation tool (Zapier, Make) moves already-structured data between apps but doesn't natively understand insurance documents. Small MGAs whose bottleneck is reading documents need the former; teams whose bottleneck is connecting apps can start with the latter.

How quickly can a small MGA actually deploy one of these platforms?

Insurance-native platforms like FurtherAI typically go live in days to a few weeks because their connectors and extraction models ship pre-trained on insurance documents. General platforms can have a first workflow running in hours, but a full intake pipeline (extraction + validation + routing) usually takes longer to build because each piece has to be assembled separately.

What does "no-code" actually mean — will we never need engineering help?

For configuration of workflows, validations, and routing rules, a no-code platform genuinely doesn't require engineering. Integrations with proprietary or legacy systems sometimes need light technical involvement — typically a few hours, not a full project — and platforms like Pipedream make that easier by allowing code only where needed.

Are these platforms compliant enough for regulated insurance workflows?

The insurance-native options (FurtherAI, Roots.ai) include audit trails, role-based access, and compliance reporting designed for insurance use cases. Power Automate and n8n have strong governance features as well. Zapier, Make, and Pipedream have basic access controls but typically require additional configuration to meet stricter MGA compliance requirements — worth confirming with your carrier paper and legal team.

How do pricing models compare?

Task- or run-based pricing (Zapier, Make, Pipedream) is cheap at low volume and scales with usage. Per-user pricing (Power Automate at $15/user/month for Premium) is predictable with team size. Self-hosted n8n is free on the community edition but has infrastructure costs. Insurance-native platforms typically price on submission volume or value processed, which tends to align cost with realized ROI.

Can no-code platforms integrate with our existing policy admin and CRM systems?

Yes. Insurance-native platforms like FurtherAI ship with pre-built connectors to common policy admin systems, CRMs, and broker portals. General platforms cover most major SaaS via standard connectors and handle the rest through webhooks or APIs.

DISCLAIMER

This article is for general informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or other professional advice. The content reflects information available as of the date of publication, and FurtherAI undertakes no obligation to update it as laws, regulations, or AI technologies evolve.

Recent posts

Ready to go further and

transform your insurance ops?

Reclaim your time for strategic work and let our AI Assistant handle the busywork. Schedule a demo to see how you can achieve more, faster.

.svg)