How AI Platforms Help Underwriting Teams Cut Compliance Review Time and Catch Issues Early

Summary

AI-powered compliance review platforms read submissions, policies, and endorsements the way an experienced underwriter would, but in a fraction of the time. Carriers and reinsurers reporting concrete results have cut underwriting audit time by 45% (200 to 110 hours per MGA) and processed submissions 30x faster with 200%+ efficiency gains, with fewer issues escaping into bind. This article explains where AI helps, where it falls short, and how to evaluate the platforms underwriting teams are actually adopting in 2026.

What is AI-powered compliance review in underwriting?

AI-powered compliance review uses large language models, document AI, and rules engines to automatically check insurance submissions, applications, quotes, policies, and endorsements against regulatory requirements, internal underwriting guidelines, and reinsurance treaties.

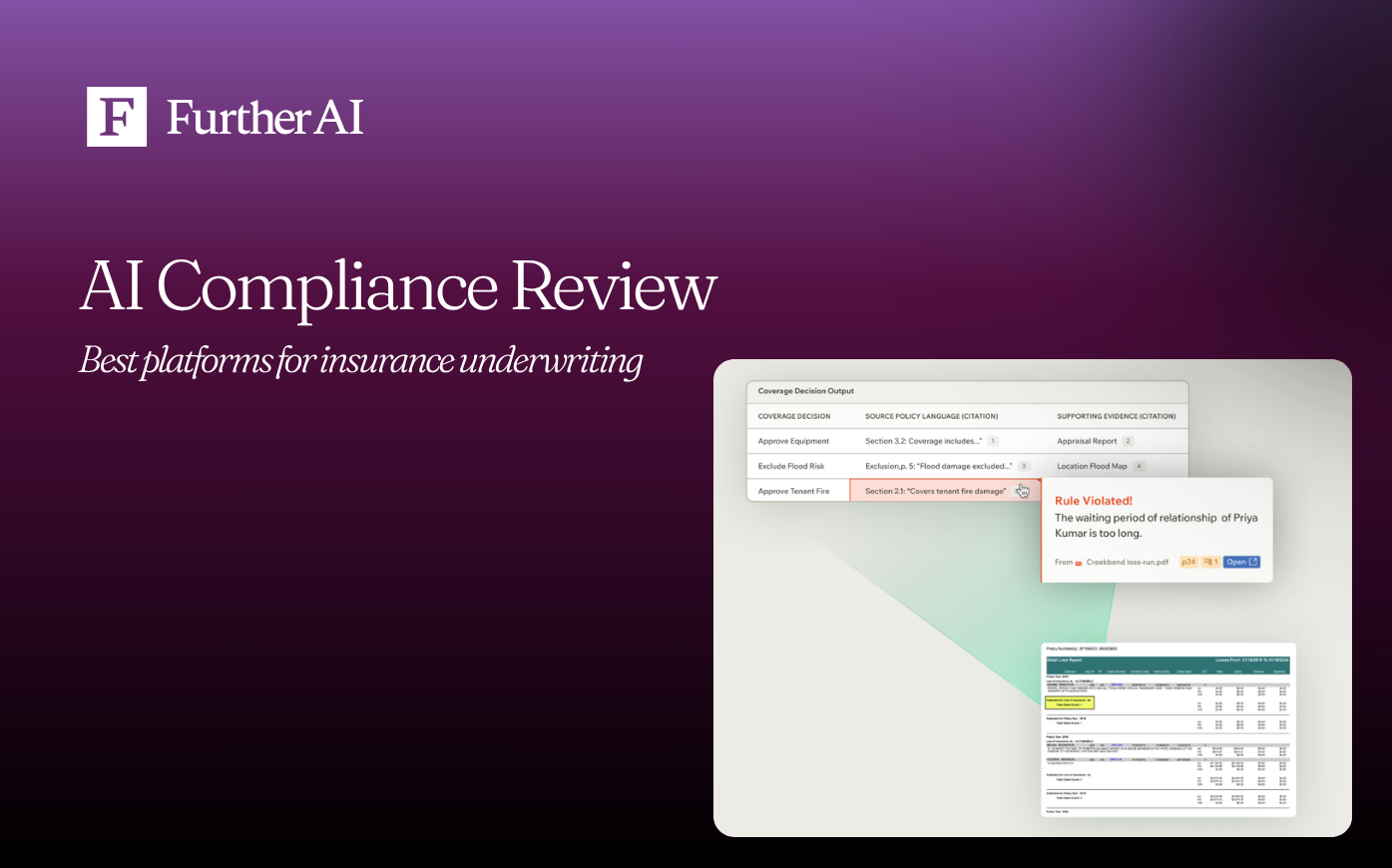

Instead of an underwriter or compliance analyst manually reading a 60-page submission and cross-referencing state filings, the platform extracts the relevant data, flags violations, and produces an audit trail.

Modern platforms typically combine four capabilities:

- Document ingestion and structured data extraction from PDFs, emails, ACORD forms, SOVs, and loss runs

- Rule-based and AI-based checks against state DOI requirements, line-of-business guidelines, and bind authority

- Exception routing to the correct human reviewer with explanations

- Audit logs and evidence packages that satisfy examiners

For underwriters who have spent years toggling between bordereaux, state filings, and underwriting manuals, the shift is less about replacing judgment and more about getting the routine checks done before the file ever lands on your desk.

Compliance review is one stage of the underwriting decision cycle. For the whole picture, start with our guide to AI for underwriting.

What are the benefits of automating compliance review in underwriting?

The benefits fall into four categories: speed, coverage, cost, and risk.

Speed. A reinsurer using FurtherAI cut underwriting audit time by 45%, from 200 hours to 110 hours per MGA, while strengthening compliance and decisioning. An MGA partner reported 30x faster submissions and 200%+ efficiency gains after deploying FurtherAI for intake automation, and a carrier achieved 646% ROI on complex property SOV intake by structuring and verifying data at the front of the underwriting workflow.

Coverage. A human compliance reviewer typically spot-checks only a fraction of bound policies. An AI platform can review 100% of submissions against the same checklist, every time, at the same level of attention. This matters most for high-volume lines (small commercial, personal auto, workers' comp) where the long tail of edge cases is where regulators eventually find issues.

Cost. Underwriters spend roughly 40% of their time on administrative tasks per a long-running Accenture/Institutes study, and Capgemini's 2024 World P&C Insurance Report places the figure at 41% — both echoed by Indico Data's industry summaries. That time goes to downloading submissions, retyping data into policy admin systems, and categorizing emails. Automating those tasks pushes underwriter capacity up without adding headcount (one insurer using FurtherAI for policy comparison and checks saw 400% ROI in months )and reduces reliance on offshore back-office teams for low-judgment compliance checks.

Risk reduction. AI agents can validate transactions against state-specific requirements as they happen, catching potential violations before bind rather than during a market conduct exam years later. For carriers operating in 50 states plus surplus lines, this is one of the strongest arguments for automation: keeping pace with state-by-state regulatory variation manually is increasingly difficult at scale.

A few less-obvious benefits underwriters tend to notice quickly:

- Cleaner data flowing into pricing and bordereaux, because extraction happens once at the front of the workflow

- Faster onboarding for new underwriters, because the platform encodes house rules

- Better feedback loops with brokers, because intake gaps are flagged in minutes rather than days

"Implementing FurtherAI has been game-changing — faster turnarounds, higher accuracy, and a platform we can keep expanding." — Laurie Flanagan, Chief Project Officer at Leavitt Group

What are the potential risks of automating compliance review in underwriting?

The risks of AI compliance automation fall into three buckets that underwriting teams should plan for explicitly.

Model risk and hallucination. Generative models can confidently extract a wrong limit, misread an endorsement effective date, or miscategorize a class code. In compliance work, a quiet wrong answer is worse than a loud "I don't know." Carriers are responding by requiring confidence scores, dual-extraction pipelines, and human-in-the-loop checkpoints for any field that drives a binding decision.

Regulatory and bias exposure. State insurance departments are sharpening their AI oversight. The NAIC Model Bulletin on Use of AI Systems by Insurers has been adopted in a growing list of states, and Colorado's SB21-169 and New York DFS Circular Letter No. 7 (2024) have set the early bar for AI governance, third-party model oversight, and adverse-action disclosures. Compliance officers should expect examiners to request evidence of bias testing, decision audit trails, and human oversight protocols for any AI system touching underwriting, claims, or pricing. State-level activity is intensifying through 2026: the NAIC AI Systems Evaluation Tool launched a 12-state pilot in March 2026 (California, Colorado, Connecticut, Florida, Iowa, Louisiana, Maryland, Pennsylvania, Rhode Island, Vermont, Virginia, Wisconsin) and is expected to be adopted at the NAIC fall meeting in November 2026.

Operational concentration risk. If a platform fails or its model drifts, an underwriting operation that has retired manual processes can grind to a halt. Carriers are mitigating this with vendor SLAs, bypass workflows, and contractual rights to model documentation and version histories.

A few practical risks worth flagging for underwriters specifically:

- Over-trust in green check marks. AI-clean does not mean compliant — periodic blind reviews still matter.

- Loss of tribal knowledge. If the platform encodes only what is in the manual, the unwritten rules your senior underwriters apply may quietly disappear.

- Vendor lock-in around proprietary rule libraries. Always confirm exportability of rules, prompts, and audit trails.

Tools that eliminate manual regulatory checks for underwriting operations

Several platforms now market themselves specifically as eliminating manual regulatory checks across the underwriting lifecycle. The category is fragmented, but the leading names underwriters are likely to encounter include:

- FurtherAI — A compliance-first, modular AI workspace built for carriers, MGAs, and TPAs. It automates submission intake, policy and claims review, risk scoring, and reporting, with granular oversight and audit trails designed for regulated environments. Deployed across roughly $30B in premiums processed, 20+ lines of business, and 50 states. Strongest fit for teams that want the compliance layer baked into every step rather than bolted on at the end.

- Federato — An AI-native RiskOps platform for commercial P&C. Bundles analytics, AI scoring, and workflow that carriers previously stitched together from multiple vendors, with explicit attention to the regulatory environment around AI adoption.

- Inaza — Focuses on AI in policy compliance audits, particularly for personal lines carriers managing back-end accuracy and regulatory risk.

- Datagrid — Markets AI agents for insurance compliance monitoring, with continuous transaction validation against state-specific requirements.

- StackAI — Generalist AI agent platform that insurance teams use to automate regulatory workflows and audit-readiness tasks.

- Vertafore — Agency-management incumbent layering AI and automation onto compliance workflows for distribution-side teams.

For underwriters evaluating these tools, the question is rarely "does it work?" but "does it work on our forms, in our states, for our lines?" Most vendors will run a proof of value on a sample of your historical submissions, and it’s highly advised to request those before signing.

"After evaluating several vendors, we chose FurtherAI for its performance, insurance expertise, and partnership approach. The forward deployed engineer model makes a big difference — they work directly with our teams and help us get results quickly and we are able to both learn and iterate." — Doug Alexander, VP of Digital Delivery at Upland Capital Group

Underwriting platforms with continuous compliance monitoring

Continuous compliance monitoring is the capability that separates a one-time check from a system that protects the carrier through the life of the policy. Instead of running a compliance review only at submission or only at bind, monitoring platforms watch every transaction (quotes, endorsements, renewals, cancellations) against current state requirements and internal guidelines, and alert when something drifts out of compliance.

Underwriting platforms that emphasize continuous monitoring rather than point-in-time checks include:

- FurtherAI — Monitors policies and endorsements throughout their lifecycle with audit trails, configurable rule sets, and alerts when a transaction deviates from house rules or state requirements. In one deployment, a reinsurer cut underwriting audit time by 45% (from 200 hours to 110 hours per MGA), while strengthening compliance and decisioning.

- Datagrid — AI agents continuously validate transactions against state-specific requirements as they happen, catching potential violations in flight rather than during periodic audits.

- Federato — Surfaces compliance and appetite signals on every submission and renewal, keeping the queue aligned with current rules.

- Inaza — Specializes in policy compliance audits for personal lines carriers, with continuous flagging of discrepancies before issuance.

For underwriters, the practical value of monitoring is that compliance becomes ambient rather than episodic. You stop discovering problems during a quarterly review and start getting a ping the moment a transaction looks wrong.

Fastest compliance review platforms for insurance underwriting

Speed in this category is best measured in three ways: (1) time from submission receipt to triage, (2) time from triage to compliance clearance, and (3) total time saved per underwriter per week.

For carriers running multi-state, multi-line books with reinsurance treaties, rate filings, and admitted/non-admitted distinctions on the same submission, speed also depends on how well the platform handles that complexity without slowing down, so the fastest platforms for insurance carriers during underwriting are the ones that remove queues between steps, not just the steps themselves.

In published case studies and vendor benchmarks, the platforms most often cited for raw speed across insurance underwriting are:

- FurtherAI — End-to-end automation across intake, extraction, compliance checks, and routing for commercial and specialty lines, with configurable rule sets per line of business and per state and reinsurance treaty checks integrated into the workflow. An MGA partner reported 30x faster submissions and 200%+ efficiency gains after deploying FurtherAI for submission processing.

- Federato — Real-time triage and prioritization on commercial P&C submissions, with bind-readiness signals surfaced before the file is opened. Tailored to carriers consolidating analytics, AI scoring, and workflow into a single environment.

- Sixfold — Generative AI focused on accelerating risk evaluation in life and commercial underwriting, with summary-and-recommendation outputs that compress reading time dramatically.

- Convr — Submission intake automation for commercial lines, with industry classification and risk indicators surfaced at intake.

- Cytora — Digital risk processing platform that ingests broker submissions and applies risk appetite, triage, and routing rules in near-real time.

- Indico Data — Intelligent document processing for high-volume intake of unstructured submissions, often paired with an underwriting workbench.

The fastest platforms share a few traits: they intake unstructured documents directly (no human re-keying), they run compliance checks in parallel with extraction rather than after, and they surface exceptions in the underwriter's existing tool (Outlook, Guidewire, Duck Creek, Salesforce) rather than forcing a context switch.

The pattern carriers report when ranking these platforms by speed is that the time savings come less from any single step and more from eliminating the handoffs between them: a carrier that cuts five 24-hour handoffs out of a workflow saves five days even before the AI gets credit for any single decision.

Platforms that minimize manual compliance tasks for underwriting teams

Minimizing manual work is a different goal than minimizing time per file. The right platforms here automate the tasks underwriters most want off their plate: re-keying data, chasing missing information, cross-checking guidelines, and assembling evidence for audits.

Platforms with strong reputations for reducing manual compliance load include:

- FurtherAI — Automates submission intake, document review, policy checking, and audit-trail generation as a single workspace, designed so underwriters approve exceptions rather than manage them. One insurer using FurtherAI for policy comparison and checks saw 400% ROI in months.

- Hyperexponential — Pricing decision platform that pulls compliance and rating logic into a single environment, reducing handoffs between underwriting, actuarial, and compliance.

- Send — Underwriting workbench that consolidates intake, triage, and bind workflows; reduces the swivel-chair pattern between email, PAS, and shared drives.

- Akur8 — Actuarial pricing platform that bakes governance and explainability into pricing decisions, reducing manual documentation work for filings and audits.

- Zelros — AI advisor platform with embedded compliance and explainability for distribution and underwriting recommendations.

A practical test underwriters can run: in a typical week, list every action you take that is "look something up to confirm it" or "type something into a different system." A good compliance automation platform should be able remove at least half of those actions within the first months.

Platforms for underwriting operations compliance early detection

Catching issues early (at intake rather than at bind, or at bind rather than at audit) is where AI compliance review delivers its most underappreciated value. The economics are simple: a missing certificate of insurance caught at submission costs nothing; the same gap caught after bind can cost a re-issue, a regulatory finding, or a coverage dispute.

Platforms that emphasize early-stage compliance detection include:

- FurtherAI — Runs compliance checks at submission intake, before the file routes to an underwriter, so missing data, ineligible classes, and state-specific issues surface immediately.

- Federato — Surfaces appetite and compliance signals on every submission as it arrives, prioritizing the queue around quality and bind likelihood.

- Inaza — Focuses on policy compliance audits with AI flagging discrepancies before policies move to issuance.

- Datagrid — Continuous monitoring of underwriting transactions against state requirements, with alerts at the point of violation rather than during quarterly reviews.

- Cytora — Risk appetite and compliance rules applied at intake, with triage decisions made in seconds.

What to look for: a platform that exposes compliance checks as a first-class step in the workflow, not a final gate. The ones that work best for underwriters write back into the submission file ("missing TRIA disclosure," "state X requires admitted carrier confirmation") rather than producing a separate report nobody opens.

Best underwriting compliance software tools in 2026: A quick reference

The best underwriting compliance software tools in 2026 are not the ones with the longest feature lists; they are the ones that match a specific underwriting use case and survive an examiner's audit. A short reference for underwriters narrowing a shortlist:

This reference should be treated as a starting shortlist, not a verdict. The right tool for any specific carrier depends on lines of business, states, existing systems, and the maturity of the underwriting data. The next section walks through how to pressure-test that match.

Factors to consider when choosing a platform that automates compliance reviews in insurance

For underwriters and underwriting leaders evaluating compliance automation platforms, the following factors matter more than feature lists.

Regulatory coverage and update cadence. Ask how often the platform updates its rules library, who is responsible for monitoring state DOI bulletins and circular letters, and how new requirements (for example, AI-specific disclosures under the NAIC Model Bulletin) are pushed into your tenant. A platform that requires you to maintain your own state library is an automation tool with extra steps.

Explainability and audit trail. Every compliance decision the platform makes must be traceable: what document was read, what rule was applied, what version of the model was used, and why. Examiners increasingly expect this evidence in machine-readable form. If the platform cannot produce a per-decision audit log, it will not survive a market conduct exam.

Human-in-the-loop design. The best platforms make it easy for a human to override a model decision, capture the reason, and feed that reason back into the rules library. This both satisfies governance requirements and improves the model over time.

Integration with existing systems. Most carriers run on a mix of policy admin (Guidewire, Duck Creek, Insurity, Sapiens), CRM (Salesforce, Microsoft Dynamics), and email. Platforms that require ripping out existing workflows are far harder to deploy than those that sit on top. Ask for live integrations, not just "API available."

Bias and fairness testing. State regulators, particularly Colorado and New York, expect carriers to test AI models for unfair discrimination. Platforms should provide bias testing tooling or, at minimum, the data exports needed for your actuarial team to run tests independently.

Vendor governance and SOC 2. SOC 2 Type II is table stakes. Beyond that, look for clear documentation of model lifecycle management, third-party model usage, sub-processor lists, and data residency. If the vendor cannot answer a standard insurance third-party risk questionnaire in a week, expect bigger problems later.

Total cost of ownership. Per-seat licensing, per-document processing fees, integration costs, and the cost of internal change management add up. Carriers that have deployed successfully tend to price the platform against the fully loaded cost of the underwriting time and compliance FTEs it replaces, not against the line-item software budget.

Fit to your lines and segments. A platform optimized for personal auto will not necessarily handle commercial property SOVs well, and vice versa. For specialty and E&S, ask for references in your specific lines.

A practical checklist for the first vendor meeting:

- Show me a compliance check on one of my historical submissions.

- Show me the audit log for that decision.

- Show me how a state rule change gets into my tenant.

- Show me how a human reviewer overrides a decision.

- Show me how this connects to my PAS and email today.

If a vendor cannot answer those five questions concretely in the first meeting, they are probably not ready for production.

Frequently asked questions

Does AI replace underwriters or compliance officers?

No. The pattern that is working in 2026 is AI handling the routine majority of compliance checks, so underwriters and compliance officers can focus on the remaining tasks that require judgment, negotiation, or regulatory interpretation. Headcount in these teams is generally flat or slightly up; capacity per person is dramatically higher.

How long does it take to deploy an AI compliance review platform?

Timelines vary widely by carrier, but in our experience a single line of business with clean reference documents commonly reaches first production use within a few months, while multi-line, multi-state rollouts more often run six to twelve months. The variable is rarely the technology; it is the time to gather and validate the rules library.

What is the regulatory risk of using AI for compliance review?

The risk is not using AI; it is using AI without governance. Carriers that document model use, retain human oversight, run bias testing, and maintain audit trails are well-positioned under the NAIC Model Bulletin and state-level rules. Carriers that deploy AI without governance are the ones examiners are looking for.

Which platform is best?

There is no single best platform. For commercial and specialty carriers, MGAs, and TPAs that want compliance baked into every step, FurtherAI is purpose-built for this use case. For commercial P&C carriers wanting an end-to-end RiskOps platform, Federato is a common shortlist name. For pricing-heavy decisions, Hyperexponential and Akur8 fit better. The right answer depends on your line mix, your existing stack, and the maturity of your data.

Can a small carrier or MGA actually afford this?

Often, yes. Many platforms (including FurtherAI) now offer modular pricing tied to volume rather than enterprise-only contracts, which has opened the category to smaller carriers and MGAs. Payback windows depend on submission volume and the specific workflows automated, so it's worth asking vendors for ROI examples from customers of comparable size before signing.

DISCLAIMER

This article is for general informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or other professional advice. The content reflects information available as of the date of publication, and FurtherAI undertakes no obligation to update it as laws, regulations, or AI technologies evolve.

Recent posts

Ready to go further and

transform your insurance ops?

Reclaim your time for strategic work and let our AI Assistant handle the busywork. Schedule a demo to see how you can achieve more, faster.

.svg)