Mixed-Format Submissions for Underwriters: Strategies 2026

The best way to handle mixed-format submissions is to stop treating each format as a separate manual task and build one unified intake workflow that classifies, extracts, and validates every document type (PDFs, Excel Schedules of Values (SOVs), ACORD forms, email threads, and scanned loss runs) before a submission ever reaches an underwriter. The goal is simple: every submission arrives decision-ready, regardless of how a broker sent it.

That matters because submissions rarely arrive in one clean format. A single new-business file might include a broker email with the real context buried in the body, an ACORD 125 application as a PDF, a 5,000-row Excel SOV, and a scanned loss run that's three years of claims history in an unsortable image. Your team's turnaround time is set by the messiest document in the stack, not the cleanest.

This guide breaks the problem down format by format, then shows how to unify them into a single intake strategy you can defend to leadership and operate at scale in 2026.

Handling messy, mixed-format submissions is one piece of a wider picture, though. Check out our complete AI underwriting guide to see where it sits in the end-to-end flow.

Key takeaways

- Mixed-format submissions slow intake because they force underwriters into data entry. Accenture found the average underwriter spends 70% of their time on non-underwriting work.

- Five formats cause most friction: broker PDFs, Excel SOVs, ACORD forms, email threads, and scanned loss runs, each needing its own handling logic.

- A unified intake pipeline beats five separate processes by classifying, extracting, validating, and summarizing every format in one pass.

- Keep humans in the loop: the strongest deployments have AI prepare the work and underwriters approve the decisions.

- Track four metrics: turnaround time, accuracy, submission-to-quote rate, and cost per submission. Small turnaround gains translate into large premium gains.

Why mixed-format submissions create underwriting bottlenecks

Mixed-format submissions create bottlenecks because they force skilled underwriters to spend their time on data entry instead of risk selection.

The scale of that drain is well documented. Accenture's long-running P&C underwriting survey, conducted with The Institutes, found that the average underwriter spends 70% of their time on non-underwriting activities, including 40% on administrative tasks like rekeying data. Underwriters themselves named redundant inputs and manual processes as the single biggest hurdle to writing business. McKinsey reports a similar pattern in large commercial operations, where 30% to 40% of underwriters' time goes to administrative tasks such as rekeying data and manually running analyses.

The root cause is that most submission data is unstructured. Industry analysis consistently estimates that around 80% of insurance data sits trapped in documents and correspondence (emails, PDFs, and scanned files) rather than in clean, queryable fields. Every format that needs manual handling adds a queue, and every queue adds days.

The bottleneck is also a revenue problem. Slow, inconsistent intake means quotes go out late, and in commercial lines the first complete quote often wins the deal. This pressure hits non-standard, high-complexity books hardest, which is why Excess & Surplus lines, where submissions are rarely standardized, feel mixed-format friction most acutely.

“From the lens of an underwriter, identification of line of business is an afterthought at time of submission receipt. Why? Because the underwriter has the individual context of “what BU they work for”. In other words, a ‘Management Liability’ underwriter knows they receive ‘Management Liability’ submissions (e.g. D&O, EPL, Fiduciary, Crime, E&O etc.).” — Ben Grosser, Head of Insurance AI at FurtherAI

The five document formats slowing your intake workflow

A mixed-format submission is any underwriting file that arrives across multiple document types at once, each requiring different handling before the data is usable. Five formats cause most of the friction. The table below summarizes them; the sections that follow give each one its own triage logic and handling strategy.

Broker PDFs and application packets

PDFs are the default submission format, and the problem is that no two brokers build them the same way. The handling strategy is to classify each PDF by document type first (application, supplemental, financial statement, narrative), then extract fields with layout-aware models instead of brittle templates that break the moment a broker changes their format.

Excel SOVs

Schedules of Values are the heaviest lift in property intake. A single SOV can run from 500 to 100,000 locations, with up to 60 data fields each, spread across multiple tabs with inconsistent headers. The strategy is automated schema mapping: align whatever the broker sent to your underwriting system's fields, then validate, geocode, and enrich every row. We'll cover a real-world SOV example in the ROI section below.

ACORD forms

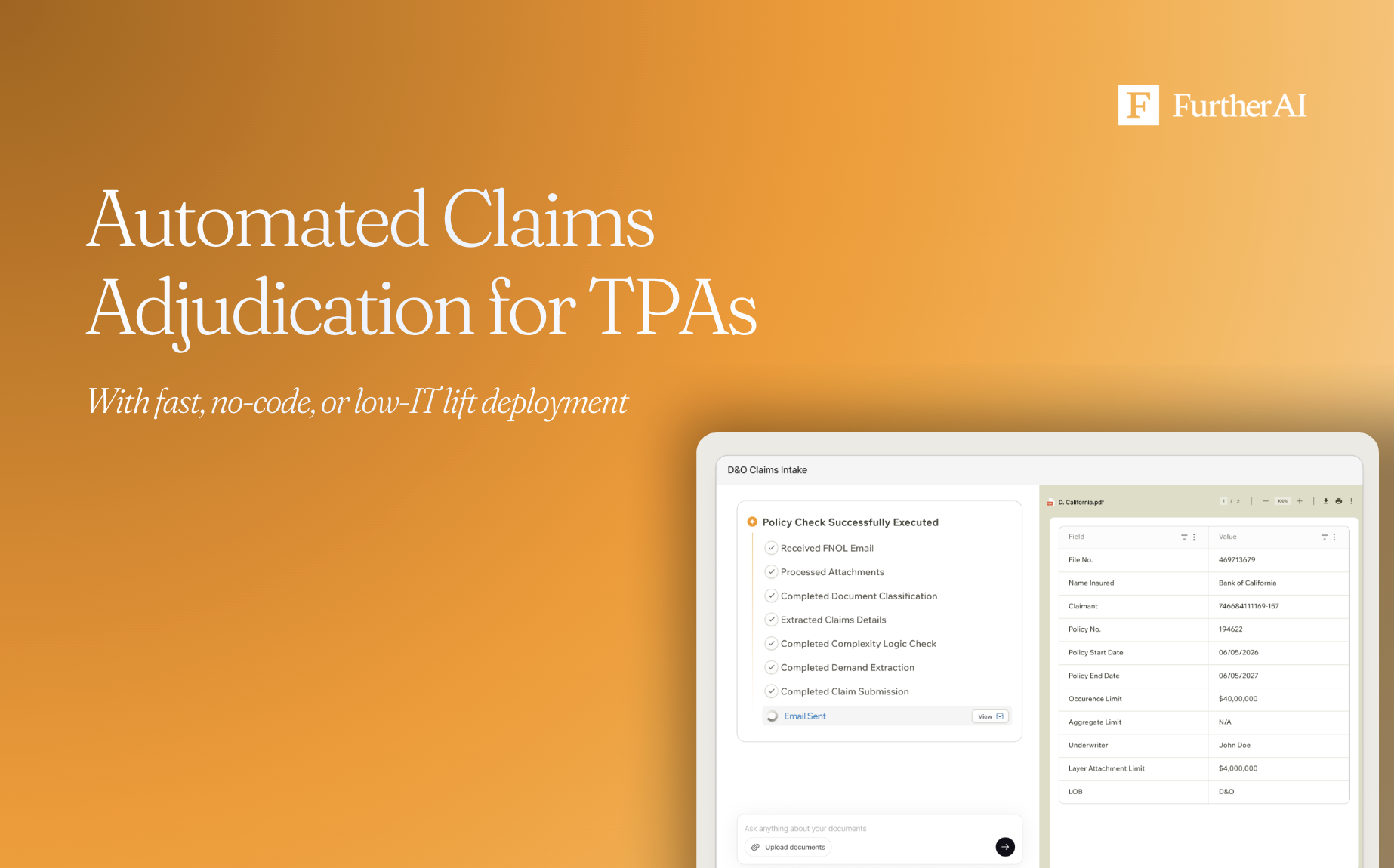

ACORD forms, like the ACORD 125 commercial insurance application and the ACORD 611 loss run request, are the closest thing the industry has to a standard, and ACORD has published them since 1971. The friction comes from partially completed forms and flat PDF exports that strip the underlying data. The strategy is to extract against known ACORD field positions and automatically flag missing or contradictory entries before the file moves forward.

Email threads

The submission email is often where the real story lives: appetite questions, target premium, and prior-carrier context. Yet it's the format teams most often ignore. The strategy is to parse the full thread, pull the relevant context, and attach it to the structured submission so an underwriter sees the narrative and the data together.

Scanned documents and loss runs

Scanned loss runs and handwritten notes are the worst offenders because they aren't machine-readable. At Leavitt Group, one of FurtherAI’s clients, a single loss run of more than 130 lines of unstructured data once took a producer hours to format by hand, and general-purpose AI tools couldn't produce usable output. The strategy is purpose-built optical character recognition (OCR) paired with validation, structuring claims history into sortable fields in minutes.

“OCR is not the automation strategy; it is one tool inside a much broader workflow. FurtherAI’s extraction layer decides how to interpret each PDF based on the document itself, then passes usable information into the downstream steps carriers rely on, such as classification, validation, enrichment, routing, exception handling, and human review.” — Ben Grosser, Head of Insurance AI at FurtherAI

Building a unified intake strategy across all submission types

The strategy that works in 2026 is a single intake pipeline that handles every format in one pass, rather than five disconnected processes. When a submission lands, the workflow should classify each attached document, extract and map the data, run validation and eligibility checks, and produce a structured, decision-ready summary, all automatically.

A unified pipeline follows five steps:

- Ingest from every channel. Pull submissions from email, broker portals, and shared drives into one queue.

- Classify each document. Identify applications, SOVs, ACORD forms, and loss runs before extraction begins.

- Extract and map to your schema. Convert each format's data into your underwriting system's fields.

- Validate and enrich. Check completeness, resolve conflicts, geocode locations, and append third-party data.

- Summarize for the underwriter. Deliver a clearance-ready file with flagged issues and recommended next steps.

This is the layer where FurtherAI's platform is purpose-built for insurance rather than adapted from a general tool. The same approach maps directly to how carriers standardize intake across product lines without forcing brokers to change how they submit.

“When a workflow reaches an AI extraction block, FurtherAI decides how to read the PDF based on the document itself. If the PDF has embedded, machine-readable text, OCR may not be needed. If the PDF is scanned, flattened, image-heavy, or otherwise not directly readable, OCR or vision-based document reading can be invoked inside the extraction layer.” — Ben Grosser, Head of Insurance AI at FurtherAI

Automation approaches for mixed-format document processing

There are three broad approaches to automating mixed-format intake, and most teams progress through them in order.

Template-based extraction is the oldest. It works when formats are predictable and breaks the moment a broker changes a layout, so it struggles with genuinely mixed submissions. Rules-based OCR with validation handles scanned documents better but still needs heavy human cleanup on non-standard files. Insurance-specific AI is the current standard: layout-aware models that classify, extract, and validate across formats, with humans reviewing flagged exceptions rather than every field.

The distinction that matters is human-in-the-loop design. The most reliable deployments keep underwriters as the decision-makers while AI prepares and structures the work. Leavitt Group, FurtherAI’s client, built its entire AI strategy this way: AI handles data-heavy preparation, and account managers review, adjust, and approve before anything moves forward. You can explore the full range of intake and review options across FurtherAI's solutions.

Measuring ROI: Key metrics for submission intake optimization

Measure intake optimization with four metrics: submission turnaround time, field-level accuracy, submission-to-quote rate, and cost per submission. These connect directly to revenue and are the numbers a business case needs.

The outcomes can be substantial. A top-10 global carrier with over $20B in gross written premium used FurtherAI's Complex SOV Intake to cut processing from 1–5 days per SOV and 2–3 week quote turnarounds down to under 10 minutes of end-to-end intake, even on SOVs exceeding 50,000 locations. Field-level accuracy started above 95% at go-live and rose to 97% within six months, producing a 646% return on investment (ROI). Across its book, FurtherAI has processed roughly $30B in premiums spanning more than 20 lines of business.

Turnaround speed feeds the metric that leadership cares about most. Insurance Quantified estimates that every 5% gain in submission-to-quote rate is worth about $100,000 in monthly premium, roughly $1.2 million a year, for a book of 1,000 submissions a month at a $10,000 average policy. Faster, cleaner intake doesn't just save labor; it lets you quote more of the business already sitting in your inbox.

Get started with smarter submission processing

Start by mapping where your current intake breaks down by format. Pull last month's submissions, sort them by document type, and measure how long each format spends in queue before an underwriter sees it. The format with the longest wait is your first automation target, and for most teams it's SOVs or scanned loss runs.

From there, pilot a unified workflow on one line of business, measure against the four ROI metrics above, and expand once the numbers hold. If you'd like to see how mixed-format intake works on your own submissions, book a demo with FurtherAI.

REFERENCES

ACORD. "ACORD Forms." ACORD. acord.org

FurtherAI. "Complex Property SOV Intake." FurtherAI. furtherai.com

FurtherAI. "Customer Stories." FurtherAI. furtherai.com

FurtherAI. "How Leavitt Group Is Using FurtherAI to Redefine Insurance Operations." FurtherAI. furtherai.com

Insurance Thought Leadership. "How AI Can Maximize Unstructured Data." Insurance Thought Leadership. insurancethoughtleadership.com

McKinsey & Company. "Insurance productivity 2030: Reimagining the insurer for the future." McKinsey & Company. mckinsey.com

Reilly, Michael. "Why Underwriters Don't Underwrite Much." Accenture Insurance Blog. insuranceblog.accenture.com

Roth, Chad. "Getting Ahead of Submission Overload: The Need for Systematic Prioritization in Commercial Lines Underwriting." Insurance Journal. insurancejournal.com

DISCLAIMER

This article is for general informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or other professional advice. The content reflects information available as of the date of publication, and FurtherAI undertakes no obligation to update it as laws, regulations, or AI technologies evolve.

Recent posts

Ready to go further and

transform your insurance ops?

Reclaim your time for strategic work and let our AI Assistant handle the busywork. Schedule a demo to see how you can achieve more, faster.

.svg)