How to Automate Underwriting Summary Creation With Audit Capabilities for MGAs

Managing general agents (MGAs) are the fastest-growing channel in U.S. property and casualty (P&C) insurance. As per strategic study by Conning, direct premiums written by U.S. MGAs reached $114.1 billion in 2024, up 15% year over year and the fourth straight year of double-digit growth. That growth has a cost: more submissions, more delegated authority, and more carrier and regulatory scrutiny on every bound policy.

To automate underwriting summary creation with audit capabilities, MGAs need a pipeline that does four things in one pass: ingests every submission channel, extracts and structures the data, applies underwriting rules with documented rationale, and writes an immutable evidence trail to each summary. Done right, the summary itself becomes the audit artifact: no separate trail to assemble at exam time.

This guide walks through how that pipeline actually works, what to build versus buy, and the KPIs that show carriers and regulators you have it under control.

Key takeaways

- Audit-ready means evidence-native. Every field in the summary should carry its source document, extraction confidence, reviewer note, and decision rationale — captured automatically, not reconstructed later.

- Build in this order: intake standardization → extraction → explainable decisioning → evidence capture → integrations → monitoring. Skipping steps creates rework.

- Regulators are explicit. The NAIC Model Bulletin on AI and the EIOPA Opinion on AI Governance (BoS-25-360) both require documented governance, traceable decisions, and explainable outputs.

- Real outcomes anchor the case. A FurtherAI MGA customer cut average time-to-clear a submission from 32 minutes to roughly one minute at near 99% accuracy, and a reinsurer cut audit time per MGA from 200 hours to about 110 hours.

Why underwriting summary automation matters for MGAs now

MGAs sit between brokers, carriers, and policyholders, and the volume on every side is rising. AM Best attributes much of the 15% jump in MGA premium to fronting growth and the migration of underwriting talent into delegated programs — both of which expand carrier oversight obligations. The 2025 Conning MGA study notes broader compliance pressure on delegated authority programs.

For most MGA ops teams, that makes manual summary creation (copying ACORD fields, retyping SOV rows, screenshotting loss runs into a Word template) an unsustainable way to defend a binding decision. Carrier audits routinely sample dozens of policies per program, and a missing extraction note or unsourced rationale can pull an entire book into remediation. McKinsey estimates underwriters lose 30–40% of their time to administrative work in large commercial lines, and Deloitte reports comparable 30–40% productivity gains where insurers have actually wired automation into underwriting workflows.

What "audit-ready" actually means

An audit-ready summary is a record where every claim, value, and decision can be traced back to its source in seconds. That requires four capabilities working together.

"Audit readiness breaks down when evidence has to be reassembled after the fact — by then, the trail is cold and the context is gone. FurtherAI solves that by embedding source-cited AI directly into the workflows that generate audit evidence in the first place, with inline citations, reviewer-in-the-loop checkpoints, and every output captured as structured data in a clean, organized record that stays queryable long after the work is done. The result is documentation that's defensible by default and instantly retrievable today or tomorrow, aligned with NAIC AI Model Bulletin expectations around traceability and human oversight." — Danny O'Lenic, Insurance Product Lead at FurtherAI

The four pillars of audit-ready underwriting automation

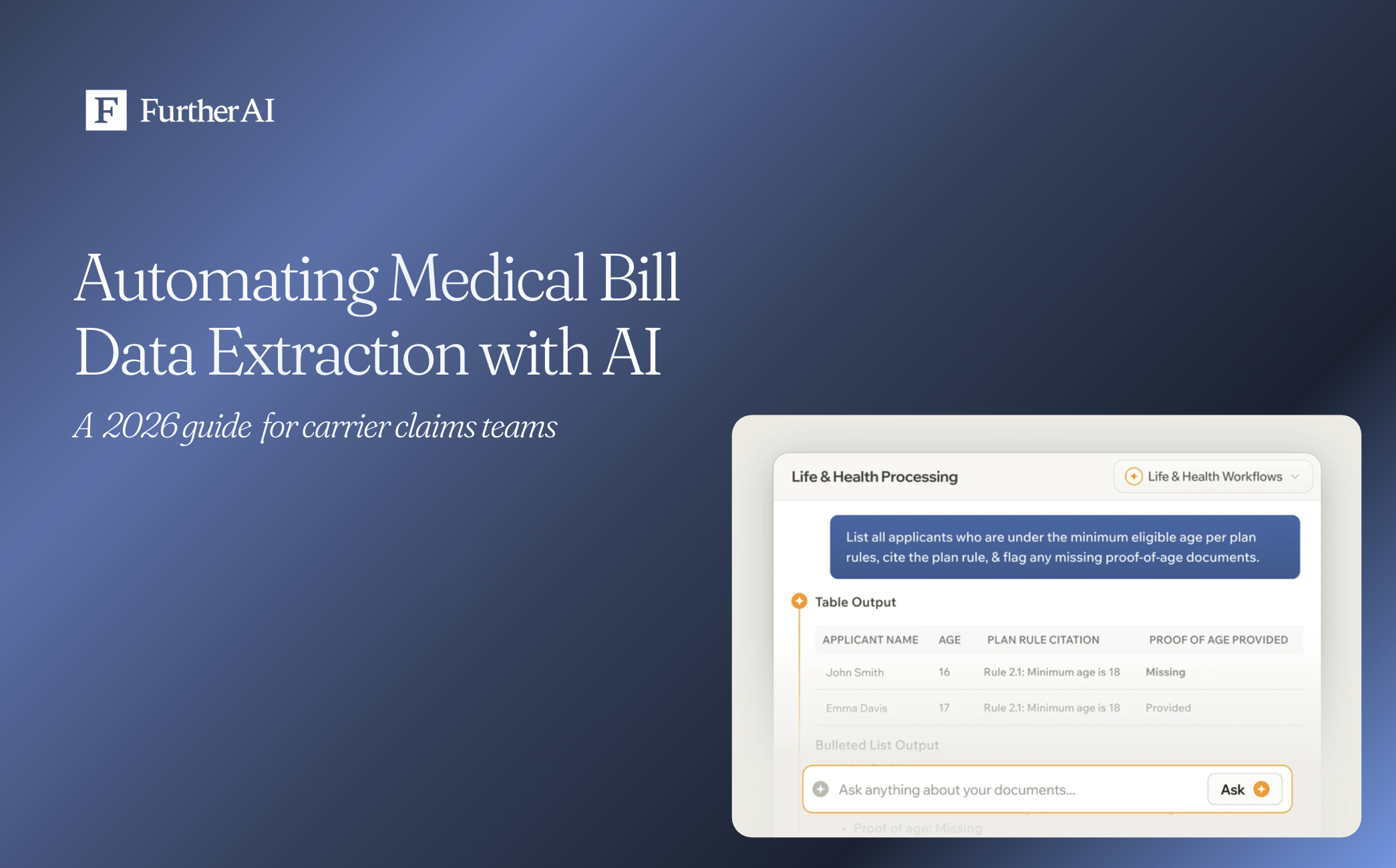

- Omnichannel intake and extraction. The pipeline ingests broker emails, portal submissions, ACORD PDFs, SOV spreadsheets, loss runs, and third-party enrichment in their native form, classifies them, and pulls structured fields with human-in-the-loop validation on low-confidence items.

- Explainable, deterministic decisioning. Eligibility, appetite, and rating logic run as documented rules — with any AI-generated rationale anchored back to source wording and the governing guideline.

- Evidence capture by default. Source files, extraction logs, timestamps, reviewer edits, and control IDs (SOC 2, ISO 27001, NAIC) attach to each summary automatically — not assembled by hand at audit time.

- Integration with the workbench, PAS, and bordereaux. Clean structured output flows into your underwriting workbench, policy admin system, and carrier reporting templates via APIs so the audit trail stays intact end to end.

A pipeline missing any one of these still produces summaries, but you'll be reconstructing the trail manually when a carrier examiner or regulator asks.

Basic automation versus audit-ready automation

A six-step implementation playbook

The order matters. Clean intake feeds clean rules; clean rules feed defensible summaries. Skip a step and you'll backfill later.

Step 1: Map the current submission-to-bind workflow

Quantify cycle times, exception sources, and rework. Pin down where underwriters and assistants are actually spending hours — typically intake parsing, SOV reformatting, and loss-run summarization. Use the McKinsey 30–40% administrative-task benchmark as a sanity check, but your own time-study will be sharper.

Step 2: Standardize intake and structure extraction

Consolidate the inbox. Route every submission — broker email, portal upload, third-party feed — through one extraction pipeline that returns ACORD fields, SOV rows, and loss-run summaries in a consistent schema. Layer large language model (LLM) extraction with domain validation; one FurtherAI MGA customer reached near 99% accuracy on property submission intake with this pattern.

Step 3: Apply explainable underwriting rules

Encode appetite, eligibility, and rating logic as deterministic rules with AI assistance for ambiguous text. Every rating, exclusion, or referral note should carry a citation to the underwriting guideline it came from. That citation is what makes the summary defensible later — and it's what both the NAIC Model Bulletin and EIOPA's 2025 AI Opinion call for.

Step 4: Attach evidence to every summary

Every summary should embed its provenance. The table below shows the minimum evidence layer carriers and auditors expect to see attached to each case.

Step 5: Integrate with workbench, PAS, and bordereaux

Open APIs into your underwriting workbench, PAS, and carrier reporting templates keep the audit trail intact end to end. Bordereaux generation is the highest-leverage integration for MGAs: clean, validated extraction means monthly reporting stops being a reconciliation project.

Step 6: Monitor, test for bias, and re-validate

Continuous monitoring catches data drift; periodic bias testing satisfies regulators that comparable risks are treated consistently. The NAIC bulletin explicitly requires a written AI governance program with documented testing and senior management accountability, as summarized in this overview of the NAIC AI Model Bulletin requirements.

KPIs that prove the model is working

Track these to show carriers, reinsurers, and your own leadership that automation is performing — and to give regulators a clean compliance story.

Benchmark from your own pre-automation numbers rather than an industry average. The point of the dashboard is to show movement on your book, not match someone else's.

What MGAs and their carriers are seeing in practice

Real outcomes from FurtherAI customers illustrate what an audit-ready pipeline produces:

- A leading MGA with over $1.5 billion in premium automated property submission intake and dropped average time-to-clear from 32 minutes to about 1 minute (30x), processed $20 billion in TIV in the first three months, and reported a 200%+ underwriting efficiency gain at near 99% accuracy. (Submissions Processing case study)

- A reinsurer auditing 100+ MGAs annually cut total audit time from approximately 200 hours per MGA to about 110 hours (a 45% reduction) by automating the data extraction and guideline-comparison portions of the audit. (Underwriting Audit case study)

- A regional insurer revamped its policy comparison workflow with FurtherAI and reported a 400% ROI within months. (Policy Comparison & Checks case study)

- A specialty P&C carrier (Upland Capital Group) adopted FurtherAI to ingest broker submissions and extract underwriting fields, with COO Katherine Walas crediting the platform for "instant clarity where we used to spend hours."

The common thread is structure: each case study shows manual extraction and comparison work converted into structured, source-linked output that carriers and auditors can verify directly.

How FurtherAI fits the audit-ready model

FurtherAI's AI workspace is purpose-built for insurance and maps to all four pillars. Submission intake handles ACORDs, SOVs, loss runs, and broker emails into one structured record. Guideline validation maps each submission to the MGA's underwriting and rating rules with clause-level citations. Policy and bordereaux workflows generate carrier-ready outputs with source-linked evidence attached. The platform is SOC 2 Type 2 compliant and ISO 27001 certified, with integrations into common workbench and PAS environments.

For MGA leaders, that means audit-readiness arrives as a property of the workflow itself — not as a separate compliance project bolted on after the fact.

Frequently asked questions

What is audit-ready underwriting summary automation?

It's a pipeline that turns a raw submission into a structured underwriting summary while automatically capturing the evidence that proves how each field and decision was reached. Every value carries its source document, extraction log, reviewer note, and rule citation, so the summary itself is the audit artifact — defensible to carriers, reinsurers, and regulators without rebuilding the trail manually.

How is this different from generic document AI or RPA?

Generic document AI extracts text; RPA moves data between systems. Audit-ready underwriting automation does both, plus it applies your underwriting rules, documents the rationale for each decision, and attaches a control-mapped evidence trail. It's the difference between a faster typing assistant and a defensible underwriting workflow — and it's the model that meets the NAIC Model Bulletin on AI.

What does the regulator actually require?

The NAIC Model Bulletin asks insurers — including MGAs operating under delegated authority — to maintain a written AI governance program, document decision logic, retain audit trails, and oversee third-party AI vendors. In Europe, EIOPA's 2025 AI Opinion adds explainability, human oversight, and reproducible audit trails. Both expect documented governance, not just disclosure.

How long does implementation actually take?

Most MGAs pilot a single program or line of business first — typically property or a specific E&S segment — to validate the intake schema and rule set. From pilot to measurable outcomes commonly runs weeks rather than quarters when the platform integrates over email and APIs without ripping out the workbench. FurtherAI customers have processed over a billion in TIV within the first few months of a single-program rollout.

What KPIs should we report to carriers and reinsurers?

Time-to-clear per submission, audit exception rate, hours per carrier audit, straight-through processing rate, and manual evidence collection time are the core five. Pair each with a pre-automation baseline so the trend is visible. Carriers care most about exception rate and evidence completeness; reinsurers focus on audit hours and consistency of decisioning across the delegated book.

Can a small or mid-size MGA actually deploy this?

Yes. Modern audit-ready platforms ingest submissions over email or a portal, integrate with existing workbenches through APIs, and don't require replacing the PAS. McKinsey's underwriting research and Deloitte's agentic AI productivity findings both note that scope discipline — one line, one channel — produces faster ROI than enterprise-wide projects for smaller carriers and MGAs.

DISCLAIMER

This article is for general informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or other professional advice. The content reflects information available as of the date of publication, and FurtherAI undertakes no obligation to update it as laws, regulations, or AI technologies evolve.

Recent posts

Ready to Go Further &

Transform Your Insurance Ops?

Reclaim your time for strategic work and let our AI Assistant handle the busywork. Schedule a demo to see how you can achieve more, faster.

.svg)