The Definitive Framework for Secure, AI‑Powered Claims Intake

AI-powered claims intake uses large language models (LLMs) and machine learning to capture First Notice of Loss (FNOL) across channels, turn unstructured files into structured data, triage and route claims, and keep a full audit trail with human review. Done well, it shortens cycle times, lowers handling costs, and strengthens compliance — all without handing high-stakes decisions to a black box.

This guide lays out the five-part framework we use at FurtherAI to deploy secure claims intake for carriers, managing general agents (MGAs), and brokers, the data behind each step, and a practical rollout checklist you can follow.

Key takeaways

- Claims intake is the bottleneck worth fixing first. Bain & Company estimates generative AI could reduce P&C loss-adjusting expenses by 20–25% and cut leakage by 30–50%, creating more than $100 billion in benefits industry-wide. McKinsey projects that routine, predictable claims — about 60% of future claim volume — will be suited for digital or automated resolution.

- Digital experience drives satisfaction. As per J.D. Power 2024 U.S. Claims Digital Experience Study, satisfaction with the digital claims process reached 871 on a 1,000-point scale in 2024 — up 17 points year over year — and digital reporting overtook the phone as the most satisfying way to file a claim; pushing customers across more than one channel cuts satisfaction by over 100 points.

- A secure framework has five pillars: multichannel FNOL, data capture and normalization, intelligent triage, fraud detection, and governance with auditability.

- The results are measurable. One specialty insurer using FurtherAI's Claim Intake reached over 90% automation, more than $360K in annual savings, and 10x faster processing (FurtherAI customer story).

What is AI-powered claims intake, and how does it work?

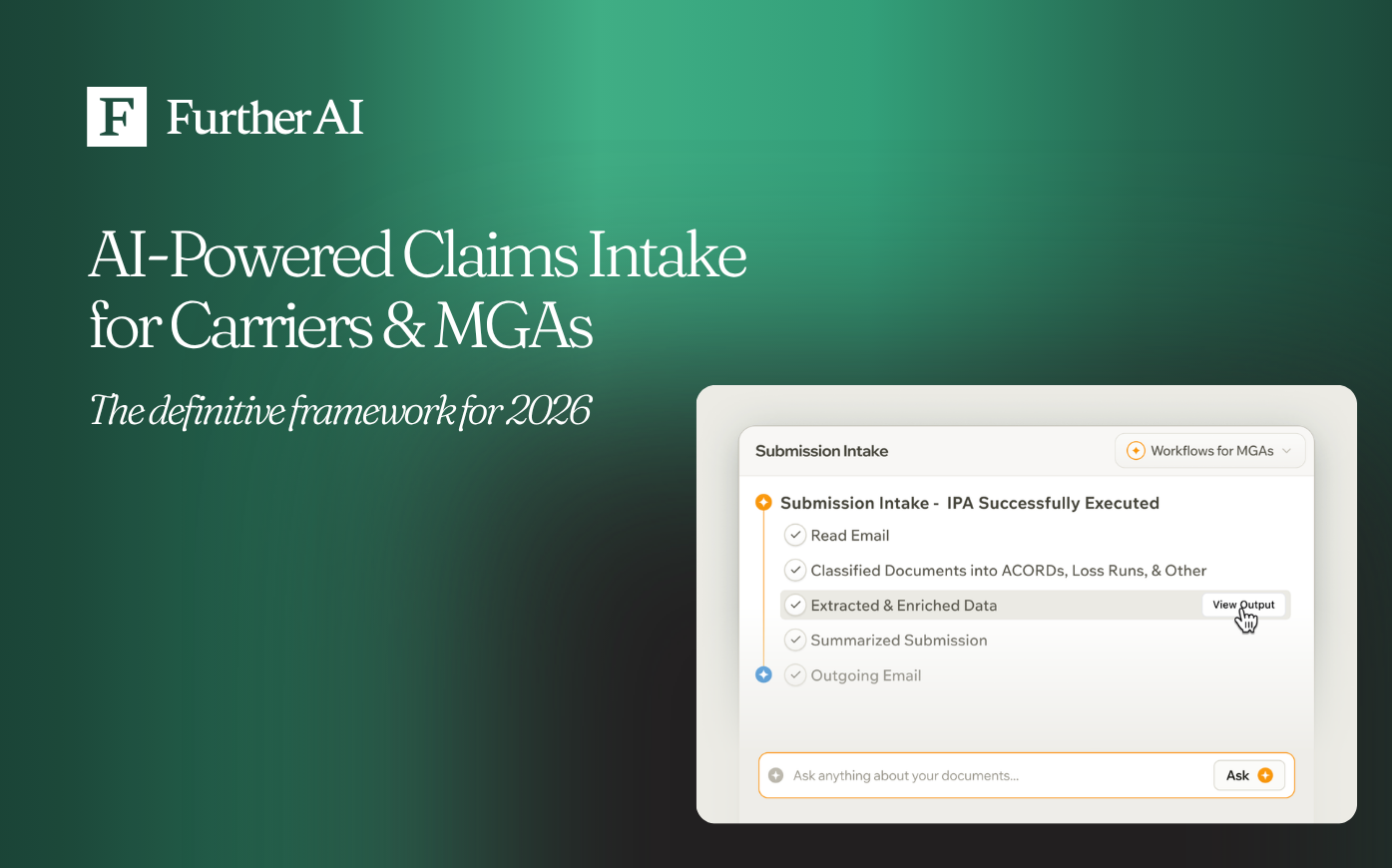

AI-powered claims intake is the automated capture, structuring, and routing of new claims using machine learning and language models. It collects FNOL across web, mobile, voice, and broker channels, extracts and normalizes data from emails, PDFs, photos, and handwritten notes, scores each claim for complexity and fraud risk, and escalates anything sensitive to a human adjuster with a clear rationale.

Here's how it works, step by step:

- Capture: the system ingests the first notice from any channel — web form, mobile app, voice, SMS, email, or a broker API.

- Extract and normalize: OCR and intelligent document processing pull fields from unstructured files and standardize them into a consistent schema.

- Validate: extracted data is checked against the policy and coverage record, and missing documents are requested automatically.

- Score and triage: each claim gets a complexity and fraud-risk score, then a specialty tag.

- Route with an audit trail: clean, low-risk claims flow straight through, while high-value or sensitive ones escalate to a human adjuster — and every action is logged.

The problem it solves is structural. Claims arrive as sprawling, inconsistent files, and manual intake forces adjusters to rekey data before any real work begins. At one specialty insurer we worked with, 98% of claim workflows were fully manual, and initial intake alone consumed roughly 2.5 hours per claim — about 7,500 labor hours a year across 3,000-plus claims (FurtherAI customer story). That model creates rekeying errors, delays first contact, and caps how fast a carrier can grow.

How carriers and MGAs automate claims intake with AI

Carriers and MGAs automate claims intake with AI by deploying the five-pillar workflow above — multichannel FNOL, data capture and normalization, intelligent triage, fraud detection, and governance — usually starting with one high-volume line, then expanding once accuracy and automation rates are proven. The fastest path to value is to target initial intake first, where work is repetitive and rules-based, before moving to adjudication.

Priorities differ slightly by role:

- Carriers focus on standardizing intake across channels and lines to expand capacity without adding headcount.

- MGAs prioritize audit-trailed document extraction and appetite-aligned routing to scale binding authority within carrier guidelines.

- Brokers use intake automation to submit complete, validated files the first time, reducing back-and-forth with carriers.

The proof is in the rollout. The specialty insurer above went from near-zero automation to more than 90% on its targeted intake workflow, cutting 2.5 hours of manual work per claim and reaching roughly 568% ROI (FurtherAI customer story). The sections below break down each pillar and a step-by-step rollout you can follow.

Core components of a secure claims intake framework

A trustworthy framework balances speed with control across five pillars. Each one maps to a specific risk: incomplete data, messy files, misrouting, fraud leakage, and regulatory exposure.

Top performers treat intake as a decision intelligence problem, not a data entry problem; they wire human-in-the-loop gates into high-risk decisions, keep end-to-end audit trails, and test on privacy-preserving synthetic data before go-live.

Multichannel First Notice of Loss capture

First Notice of Loss is the moment a policyholder first reports a potential claim — the event that triggers the entire claims lifecycle. Expanding FNOL options improves data quality, cuts back-and-forth, and lifts satisfaction, because the way a claim starts shapes how fast it closes.

The customer data backs this up. Digital reporting has overtaken phone as the most satisfying way to file a claim, yet insurers still deliver adequate digital status updates only 22% of the time, as per J.D. Power 2025 U.S. Claims Digital Experience Study. Closing that gap is one of the highest-leverage moves in intake.

A strong channel mix includes:

- Web and mobile smart forms that adapt follow-up questions to claimant inputs, reducing incomplete submissions.

- Conversational AI over voice and SMS for hands-free reporting, language support, and accessibility.

- APIs that ingest broker-to-carrier submissions directly from core systems.

Data capture and normalization technologies

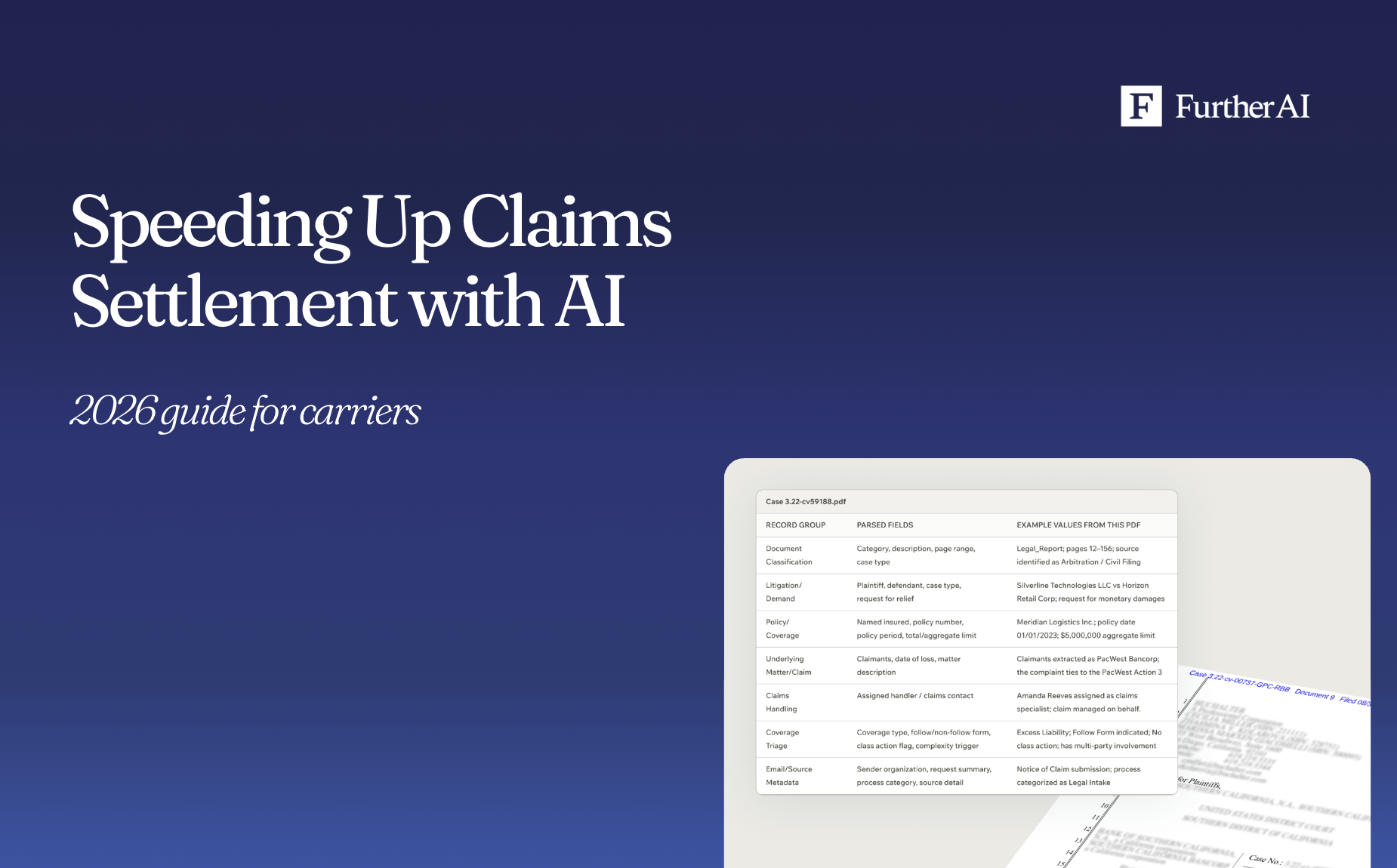

Turning unstructured claims data into clean, structured fields is the foundation everything else sits on. Two technologies do the heavy lifting: optical character recognition (OCR), which converts typed or handwritten text in images and PDFs into machine-readable text, and intelligent document processing (IDP), which classifies documents, extracts fields, and applies validation rules across diverse sources.

EY's work shows the payoff. Using OCR and natural language processing, EY teams converted semi-structured and unstructured documents into structured data for a Nordic insurer, lifting operational efficiency and improving the customer experience (EY case study). Similarly, Deloitte notes that generative AI eases the burden of summarizing and synthesizing claim data so front-line professionals can decide faster.

Match the file type to the right extraction approach:

Intelligent triage and routing

Intelligent triage uses complexity scoring to route each claim to the right handler, reserving human expertise for high-risk or atypical cases. Straightforward, low-complexity claims can move through automatically, while high-value or unusual ones escalate with a documented rationale.

A simple decision flow looks like this:

- Run AI intake and data normalization.

- Generate a complexity and risk score, and tag the specialty.

- Route on the score:

- Below threshold: auto-assign to straight-through processing.

- Borderline or high-value: escalate to a human adjuster with reasons.

- Regulatory-sensitive: auto-hold for compliance review.

This is where speed shows up for the customer. Because settlement satisfaction falls sharply after three weeks, getting clean claims onto the right desk on day one protects both the loss ratio and the relationship.

Fraud detection and authenticity verification

Fraud detection uses machine learning to flag suspicious patterns, inconsistencies, and forged documents for Special Investigation Unit (SIU) review — reducing leakage without burdening honest claimants. The stakes are large: insurance fraud costs the U.S. an estimated $308.6 billion a year, with property and casualty fraud accounting for roughly $45 billion of that total, as per Coalition Against Insurance Fraud; Insurance Information Institute.

The opportunity is just as large. Deloitte projects that AI deployed across the claims lifecycle could help P&C insurers prevent fraud and save between $80 billion and $160 billion by 2032. Common controls include:

- Anomaly detection on claim amounts, timing, and frequency.

- Image and video forensics, metadata checks, and evidence tagging.

- Cross-template and duplicate-content checks to catch altered or reused documents.

- Integration with external fraud databases for enrichment.

Governance, auditability, and compliance controls

Auditability means every automated decision is logged, explainable, and reviewable. Regulators now expect it. The National Association of Insurance Commissioners (NAIC) adopted its Model Bulletin on the Use of Artificial Intelligence Systems by Insurers in December 2023, and as of March 2025 roughly two dozen states had adopted it. The bulletin asks insurers to maintain a written AI Systems Program built on transparency, fairness, and accountability (NAIC Model Bulletin, PDF).

Recommended controls:

- End-to-end audit trails with reason codes for every decision.

- Role-based access control (RBAC), single sign-on (SSO), and multi-factor authentication (MFA).

- Immutable event logging and time-stamped evidence.

- Documented appeal and adverse-action pathways.

- Annual vendor security and compliance attestations, such as SOC 2.

FurtherAI in action: Claims intake outcomes

We treat intake as a decision intelligence problem, and the results show up in the numbers. A specialty insurer with three consecutive years of more than 20% premium growth deployed FurtherAI's Claim Intake to clear a workflow bottleneck that threatened to throttle its expansion.

Source: FurtherAI Claims Processing customer story.

These gains extend across the value chain. FurtherAI customers have reached 30x faster submissions with 200%-plus efficiency gains, a 45% cut in underwriting audit time, and 646% ROI on complex property statement-of-values intake. Across the platform, FurtherAI has processed roughly $30 billion in premiums across 20-plus lines of business in 50 states.

Step-by-step implementation checklist

A phased rollout reduces risk and gets you to value faster:

- Plan. Define target lines, volumes, service-level agreements, and risk thresholds; map integration points and data governance.

- Configure technology. Enable FNOL channels, set up OCR and IDP, vector search, and workflow rules.

- Build workflows. Design triage thresholds, fraud checks, and human-in-the-loop gates.

- Test. Use sandboxed environments and synthetic data to validate accuracy, fairness, and failure modes before go-live.

- Roll out. Pilot one line or channel, measure KPIs, and calibrate thresholds.

- Optimize. Expand coverage, monitor for model drift, and codify governance updates.

Monitoring KPIs and continuous improvement

Set up monthly dashboards and quarterly reviews so you can spot trends and tighten controls. Track turnaround time, error rates, and automation rate to quantify results.

How to select the right AI claims intake solution

Use a focused buyer's checklist. The strongest vendors prove enterprise-scale accuracy and integrate cleanly with your core systems:

- Security and compliance: SOC 2 attestation, audit trails, SSO and MFA, alignment with the NAIC AI bulletin.

- Integrations: native connectors to core claims suites, broker portals, and third-party data providers.

- Data extraction: coverage for PDFs, emails, and images, with confidence scoring and personally identifiable information (PII) redaction.

- Triage flexibility: configurable thresholds, reason codes, and human-in-the-loop gates.

- Speed-to-value: rapid deployment, low-code configuration, and managed change support.

- Customer experience: real-time status APIs, self-service portals, and multilingual support.

FurtherAI is purpose-built for commercial insurance and delivers on each of these through modular, integration-ready AI assistants — backed by audited customer outcomes and a $25 million Series A led by Andreessen Horowitz.

Frequently asked questions

What is AI-powered claims intake and how does it work?

AI-powered claims intake automatically captures, structures, and routes new claims using machine learning and language models. It works in five steps: capture FNOL across channels, extract and normalize data from unstructured files with OCR and intelligent document processing, validate it against the policy, score each claim for complexity and fraud risk, then route — clean claims straight through and sensitive ones to a human adjuster, with every action logged.

How do carriers and MGAs automate claims intake with AI?

They deploy a five-pillar workflow — multichannel FNOL, data capture and normalization, intelligent triage, fraud detection, and governance — and start with one high-volume line, usually initial intake. Carriers standardize intake to expand capacity, MGAs prioritize audit-trailed extraction and appetite-aligned routing, and brokers submit complete files faster. One specialty insurer using FurtherAI reached over 90% intake automation and roughly 568% ROI.

How much can AI improve claims intake speed and cost?

Bain & Company estimates generative AI could cut P&C loss-adjusting expenses by 20–25% and leakage by 30–50%, and McKinsey expects about 60% of future claim volume to be suited for digital or automated resolution. Real deployments go further: one specialty insurer using FurtherAI reached over 90% intake automation and 10x faster processing, while digital reporting has become the most satisfying way for customers to file a claim.

How does AI detect fraud during claims intake?

AI scores claims for anomalies in amount, timing, and frequency, runs image and metadata forensics to spot altered or reused photos, and cross-checks documents against known templates and external fraud databases. Suspicious files route to the Special Investigation Unit with reason codes. Deloitte projects AI fraud tools could save P&C insurers $80–160 billion by 2032.

How do you balance automation with human oversight?

Set complexity and risk thresholds that decide each claim's path. Low-risk, routine claims flow through straight-through processing, while high-value, atypical, or denied claims escalate to expert adjusters with a documented rationale. Regulatory-sensitive claims auto-hold for compliance review. This keeps speed high on simple work and keeps judgment human where stakes are real.

What compliance standards apply to AI in claims?

Insurers should align with SOC 2 for security controls and, increasingly, the NAIC Model Bulletin on the Use of AI Systems, adopted in December 2023 and live in roughly two dozen states by early 2025. The bulletin expects a written AI governance program emphasizing transparency, fairness, and accountability, plus immutable logging and documented appeal pathways.

What metrics should I track to measure claims intake success?

Track time-to-first-contact, average resolution time, extraction accuracy, automation rate, leakage per claim, and claimant Net Promoter Score. Review them monthly on a dashboard and quarterly in depth. Accuracy and automation rate confirm efficiency; leakage and resolution time confirm you haven't traded quality for speed.

Ready to go further?

See how FurtherAI turns manual claims intake into a secure, automated workflow built for commercial insurance. Schedule a demo.

DISCLAIMER

This article is for general informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or other professional advice. The content reflects information available as of the date of publication, and FurtherAI undertakes no obligation to update it as laws, regulations, or AI technologies evolve.

Recent posts

Ready to go further and

transform your insurance ops?

Reclaim your time for strategic work and let our AI Assistant handle the busywork. Schedule a demo to see how you can achieve more, faster.

.svg)